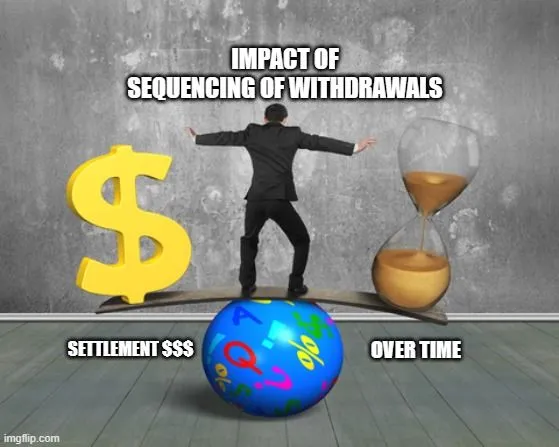

A Nasty Problem for Those Receiving Settlements

Sequencing risk and the impact of early spending after settlement

#sequencingofreturns #sequencingofwithdrawals #sequenceofreturns

Without proper settlement plannning and wealth orientation, both investment and longevity risks rest with the individual. Considering the unique human life transition experience of the plaintiff, from their life-altering event to receiving their recovery, is easy to see where things can go wrong. Unfortunately, this is not always evident if the perspective is unclear.

Experiencing a market decline in the early years following settlement can create serious problems extend beyond the immediate decrease in value of your invested settlement proceeds. Such a decline in account value, combined with excessive withdrawals, could result in a situation where your settlement proceeds might not last as long as you planned. If you have no other means support yourself, possibly with significant medical needs, and lack available family resources or support, that could prove catastrophic.

What is Decumulation?

Sequencing and Decumulation risk is a factor for recipients of legal settlements and should be addressed in advance of settlement

- Retirement planning (and I am adding settlement planning)involves grappling with two major uncertainties: Investment Uncertainty and the variability of investment returns.

- Mortality Uncertainty: The unpredictability of lifespan.

- As a Certified Financial Transitionist I am going to add identifying Transition Traits that are unique to each person and each transition and applying the appropriate collaboraive tools to

The core of the challenge lies in striking a delicate balance between three essential aspects:

- Current Needs and Wants: Ensuring sufficient income to meet immediate financial requirements, including day-to-day expenses and desired lifestyle choices.

- Long-Term Sustainability: Ensuring that the accumulated wealth (through savings, settlement proceeds and investments thereon) lasts throughout one’s lifetime, even as life expectancy and potential investment returns remain uncertain.

- The personal side of money: Personal values and processes and how this impacts decisions and outcomes.

For recipients of legal settlements, some financial products such as structured settlement annuities (like annuities with cost-of-living adjustments) can mitigate investment uncertainty and address mortaliuty risk.

Further Reading that May Be Helpful

- Monte Carlo Simulation/Analysis in Structured Settlements and Settlement Planning Process (4structures.com)

- A Personal Injury Victim’s Dilemma | Lending Settlement Money (4structures.com)

- The Passage Stage of Financial Transitions (4structures.com)

- Market Based Structured Settlements | How They Work (4structures.com)

Tools to Assess Sequencing Risk

FI Calc is a free online simulation program/calculator that evaluates retirement plans using historical data. It is particularly useful to gain an undertstanding of the impact of varying withdrawal sequencing, mixes of investments and duration. To get started, change the Retirement Plan options to see how it affects the Results.